Australian summerfruit thrives in warm, dry conditions with well-drained soil, access to irrigation water, and sufficient winter cold hours (known as chilling hours) to break dormancy. The industry spans six states across more than 26 growing regions, with production concentrated in Victoria and New South Wales. ¹

The season progresses from north to south. Early fruit arrives from subtropical Queensland and the northern growing areas of Western Australia and New South Wales from October, followed by mid-season production from the Goulburn Valley, Sunraysia, and the Riverland. Cool-climate Tasmania completes the season through to April. ²

Production by State

Victoria produces approximately 70% of national summerfruit volume, with New South Wales at 10%, Western Australia 8%, South Australia 7%, Queensland 4%, and Tasmania 1%. ³

For nectarines and peaches specifically, the 2023/24 season confirms Victoria’s production at 55,455 tonnes: approximately 76% of national nectarine and peach production of 72,813 tonnes. ⁴

Key Growing Regions by State

Victoria. Australia’s largest summerfruit-producing state. Key regions include the Goulburn Valley (Shepparton, Cobram, Tatura, Ardmona), Sunraysia (Swan Hill, Mildura), and the Murray Valley. Victoria leads peach and nectarine production and is the primary growing region for apricots. ²

New South Wales. Key regions include Young, Orange, the central tablelands, and the Murray–Darling basin. Summerfruit production is strong across peaches, nectarines, and plums. ²

South Australia. The Riverland region (Renmark, Loxton, Waikerie) is the primary production zone, with particular strength in apricots. ²

Western Australia. The Perth Hills and Chittering Valley are key growing areas, particularly for early-season fruit. WA has a distinct seasonal advantage for export windows due to its earlier harvest timing. ²

Queensland. Stanthorpe in the Granite Belt is the primary production zone, with a cool-climate microclimate at altitude supporting later-season fruit. ²

Tasmania. A smaller producing region, with the cool climate producing late-season fruit of exceptional flavour. ²

Low, medium, and high chill varieties

All summerfruit require a period of winter cold to break dormancy, measured as accumulated hours below 7°C. Low-chill varieties (suited to Queensland and coastal WA) produce fruit with fewer than 300 chilling hours; high-chill varieties (grown in southern NSW, Victoria, SA, and Tasmania) require 600 or more. This range of chill requirements is a key reason Australia can supply fresh summerfruit across the full six-month October–April window. ⁵

Sources:

¹ Austrade, Australian Summerfruit Industry Capability Report (2022)

² Austrade (2022); Plant Health Australia, Biosecurity Plan for the Summerfruit Industry (2019)

³ Hort Innovation, Summerfruit Strategic Investment Plan 2022–2026 (citing Horticulture Statistics Handbook 2019/20)

⁴ Hort Innovation, Summerfruit SARP (June 2025), citing Horticulture Statistics Handbook 2023/24

⁵ AgriFutures Australia (2017), cited in PHA Biosecurity Plan (2019)

Australia grows more than 380 varieties of summerfruit across peaches, nectarines, plums, and apricots. This diversity, combined with the geographic spread from subtropical Queensland to cool-climate Tasmania, is what makes a six-month fresh season possible. ⁴

Yellow and White Flesh

Both peaches and nectarines come in yellow and white flesh varieties, each with distinct flavour profiles, texture, and market appeal. Yellow flesh varieties tend to be sweet–tart with a firmer bite; white flesh varieties are lower in acid, floral in flavour, and more delicate in texture. The diversity of varieties within each category enables Australian growers to supply export markets with continuous supply across the season. ⁴

Plum Diversity

Plums are the most diverse of the summerfruit category in terms of skin colour, size, and flavour, ranging from yellow and green varieties through to deep red and near-black skinned fruit. Australian plum varieties include Black Diamond, Black Amber, Amber Jewel, Fortune, Angeleno, and the Queen Garnet, a Queensland-bred plum with exceptionally high anthocyanin content that has attracted international research interest. ⁵ ⁷

Apricots

Apricots occupy the shortest window in the summerfruit calendar, with peak season typically November through January. South Australia’s Riverland is the primary production zone. Australian apricot varieties include Moorpark, Trevatt, Goldrich, and a range of locally bred modern varieties.

Peaches and Nectarines

Peaches and nectarines together account for the majority of Australian summerfruit production and export volume. The season runs from October to April, supported by the full chill-requirement spread across states.

Sources:

⁴ Austrade, Australian Summerfruit Industry Capability Report (2022); SAL Variety Chart (summerfruit.com.au)

⁵ Netzel et al. (2012), Urinary excretion of antioxidants in healthy humans following Queen Garnet plum juice ingestion; Fanning et al. (2014), cited in Taylor & Francis: Nutritional Quality and Bioactive Constituents of Six Australian Plum Varieties (2020)

Australia exports summerfruit to more than 39 countries, with Asian markets accounting for the large majority of export volume and value. Australia’s counter-seasonal position relative to the northern hemisphere is a key commercial advantage: fresh Australian summerfruit arrives in Asian markets during their winter, commanding a premium over competing origins. ⁶

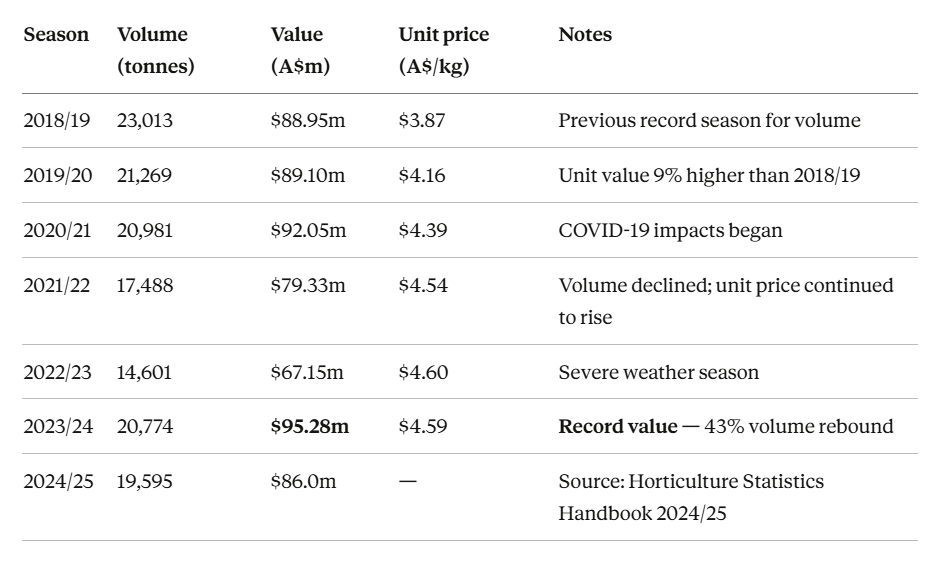

The 2023/24 season delivered a record export value of A$95.28 million: the highest in the industry’s history, despite not reaching the volume record of 2018/19. This reflects the consistent rise in unit prices from A$3.87/kg in 2018/19 to A$4.59/kg in 2023/24, demonstrating the growing premium market positioning of Australian summerfruit. ¹⁰

Victoria dominates export volumes. In 2023/24, Victoria exported 17,099 tonnes: 82.3% of the national total: up 49% on the prior season. NSW exported 3,048 tonnes (14.7% share), also up 49%. Together these two states accounted for 97% of exported summerfruit volume. ¹⁰

Variety Mix in Exports (2023/24)

By volume, nectarines accounted for 43% of summerfruit exports, peaches 22%, plums 34%, and apricots 1%. ¹⁰

Export Infrastructure

As at 2023/24, the Australian summerfruit export industry comprises 89 accredited export businesses across 2,723 hectares of accredited land and 58 registered packhouses. Protocol markets requiring farm and packhouse accreditation prior to export are China, Taiwan, Thailand, and Vietnam. ¹⁰ ¹²

Australia’s Competitive Position

Australia’s key advantages in export markets are biosecurity standards, paddock-to-plate traceability, counter-seasonal supply, and eating quality. Australian summerfruit commands a significant price premium over competing origins in Asian markets.

Chile is Australia’s primary competitor in Asian summerfruit markets. Australia currently holds approximately 10% of Southern Hemisphere summerfruit trade into Asia: a share with significant room to grow, supported by the industry’s 40,000-tonne export target by 2030. ¹⁰

Export Growth Target

The Australian summerfruit industry has set a goal of reaching 40,000 tonnes of annual exports by 2030: approximately double recent seasonal volumes. Market access and market development are the two highest priorities for achieving this target. ¹⁰

Sources:

⁶ Austrade, Australian Summerfruit Industry Capability Report (2022)

¹⁰ SF19000 Final Report, Hort Innovation (SF19000 Summerfruit Market Access & Trade Development Project)

¹¹ Hort Innovation, Australian Horticulture Statistics Handbook 2024/25 (Trade section, year ending June 2025)

¹² DAFF, Industry Advice Notice 2024-35: Applications for export of summerfruit to protocol markets (agriculture.gov.au)